Nasdaq Stock Market

All the files of this project are saved in a GitHub repository.

Objective

This analysis aims to understand the relationship between 103 Nasdaq stocks, considering their average daily return and volatility.

The data is downloaded from Yahoo! Finance, for the past 20 years starting from 14 August 1999.

Packages

This analysis requires these R packages: readxl, tidyr, data.table, BatchGetSymbols, ggplot2, gridExtra, ggrepel, factoextra.

Data Download

The data is downloaded using the method BatchGetSymbols from the package BatchGetSymbols, using the list of stocks in the Excel file nasdaq_symbols.xlsx. The resulting dataframe contains stock market figures per day for each of the 103 stocks.

nasdaq_stock_list <- read_excel('data_input/nasdaq_symbols.xlsx')

dl_stock_data <- BatchGetSymbols(tickers = nasdaq_stock_list$Symbol,

first.date = first_date,

last.date = last_date,

freq.data = freq_data,

thresh.bad.data = thresh.bad.data)

## price.open price.high price.low price.close volume price.adjusted

## 1 21.05 21.40 19.10 19.30 961200 18.48912

## 2 19.30 20.53 19.20 20.50 5747900 19.63870

## 3 20.40 20.58 20.10 20.21 1078200 19.36088

## 4 20.26 21.05 20.18 21.01 3123300 20.12728

## 5 20.90 21.75 20.90 21.50 1057900 20.59668

## 6 21.44 22.50 21.44 22.16 1768800 21.22896

## ref.date ticker ret.adjusted.prices ret.closing.prices

## 1 2005-09-27 AAL NA NA

## 2 2005-09-28 AAL 0.06217602 0.06217622

## 3 2005-09-29 AAL -0.01414645 -0.01414639

## 4 2005-09-30 AAL 0.03958461 0.03958442

## 5 2005-10-03 AAL 0.02332193 0.02332223

## 6 2005-10-04 AAL 0.03069805 0.03069767

Note that among the 103 Nasdaq stocks, 33.01 % didn’t have complete information on the selected period. The table below lists the concerned stocks and the percentage of available data. However, the missing data shouldn’t be impacting our analysis, as we will consider the average values on the period.

## Stock Code Stock Name Data %

## 1 AAL American Airlines Group Inc 69 %

## 2 ALGN Align Technology Inc 92 %

## 3 AVGO Broadcom Inc 50 %

## 4 BIDU Baidu Inc 70 %

## 5 CHTR Charter Communications Inc 48 %

## 6 CTRP Ctrip.Com International Ltd 78 %

## 7 ESRX Express Scripts Holding Co 96 %

## 8 EXPE Expedia Group Inc 70 %

## 9 FB Facebook 36 %

## 10 FOX Twenty-First Century Fox Inc 99 %

## 11 FOXA Twenty-First Century Fox Inc 99 %

## 12 GOOG Alphabet Class C 74 %

## 13 GOOGL Alphabet Class A 74 %

## 14 ILMN Illumina Inc 95 %

## 15 ISRG Intuitive Surgical Inc 95 %

## 16 JD JD.com Inc 26 %

## 17 KHC Kraft Heinz Co 20 %

## 18 LBTYA Liberty Global PLC 76 %

## 19 LBTYK Liberty Global PLC 69 %

## 20 MDLZ Mondelez International Inc 90 %

## 21 MELI MercadoLibre Inc 60 %

## 22 NFLX Netflix Inc 86 %

## 23 NTES NetEase Inc 95 %

## 24 NXPI NXP Semiconductors NV 45 %

## 25 PYPL PayPal Holdings Inc 20 %

## 26 QRTEA Qurate Retail Inc 7 %

## 27 SHPG Shire PLC 97 %

## 28 STX Seagate Technology PLC 83 %

## 29 TMUS T-Mobile US Inc 61 %

## 30 TSLA Tesla Inc 45 %

## 31 ULTA Ulta Beauty Inc 59 %

## 32 VRSK Verisk Analytics Inc 49 %

## 33 WDAY Workday Inc 34 %

## 34 WYNN Wynn Resorts Ltd 84 %

Data Preparation

For this analysis, we use the Closing Price (price.close) which is the last price of the stock at the market closure. We calculate the difference compared to the Closing Price of the previous day, and compute it to a change ratio:

The resulting dataframe looks like this:

## stock_code ref.date price.close daily_diff daily_return

## 1: AAL 2005-09-27 19.30 NA NA

## 2: AAL 2005-09-28 20.50 1.200001 0.062176221

## 3: AAL 2005-09-29 20.21 -0.290001 -0.014146390

## 4: AAL 2005-09-30 21.01 0.800001 0.039584416

## 5: AAL 2005-10-03 21.50 0.490000 0.023322228

## ---

## 460773: XLNX 2019-08-02 110.18 -3.279999 -0.028908858

## 460774: XLNX 2019-08-05 107.01 -3.169998 -0.028771084

## 460775: XLNX 2019-08-06 105.66 -1.349998 -0.012615624

## 460776: XLNX 2019-08-07 104.92 -0.740006 -0.007003653

## 460777: XLNX 2019-08-08 109.84 4.919998 0.046892853

We then aggregate the values to calculate the Average Daily Return and the Volatility (i.e. standard deviation) for each stock:

## stock_code stock_name daily_return_mean

## 1: AAL American Airlines Group Inc 0.0009913384

## 2: AAPL Apple Inc 0.0012567556

## 3: ADBE Adobe Inc. 0.0010287211

## 4: ADI Analog Devices Inc 0.0006692107

## 5: ADP Automatic Data Processing Inc 0.0004503575

## ---

## 99: WDAY Workday Inc 0.0010753307

## 100: WDC Western Digital Corp 0.0012089694

## 101: WYNN Wynn Resorts Ltd 0.0009700915

## 102: XEL Xcel Energy Inc 0.0003490931

## 103: XLNX Xilinx Inc 0.0006268699

## daily_return_sd Data %

## 1: 0.04216769 69 %

## 2: 0.02595867 100 %

## 3: 0.02757136 100 %

## 4: 0.02688987 100 %

## 5: 0.01533434 100 %

## ---

## 99: 0.02333052 34 %

## 100: 0.03788840 100 %

## 101: 0.03055400 84 %

## 102: 0.01663284 100 %

## 103: 0.02838089 100 %

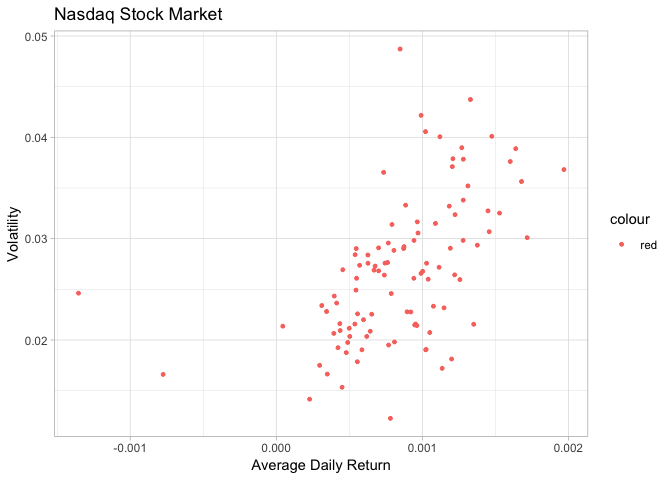

This last table will be the basis for our cluster analysis. We can visualize the information as below:

Cluster Analysis: K-Means

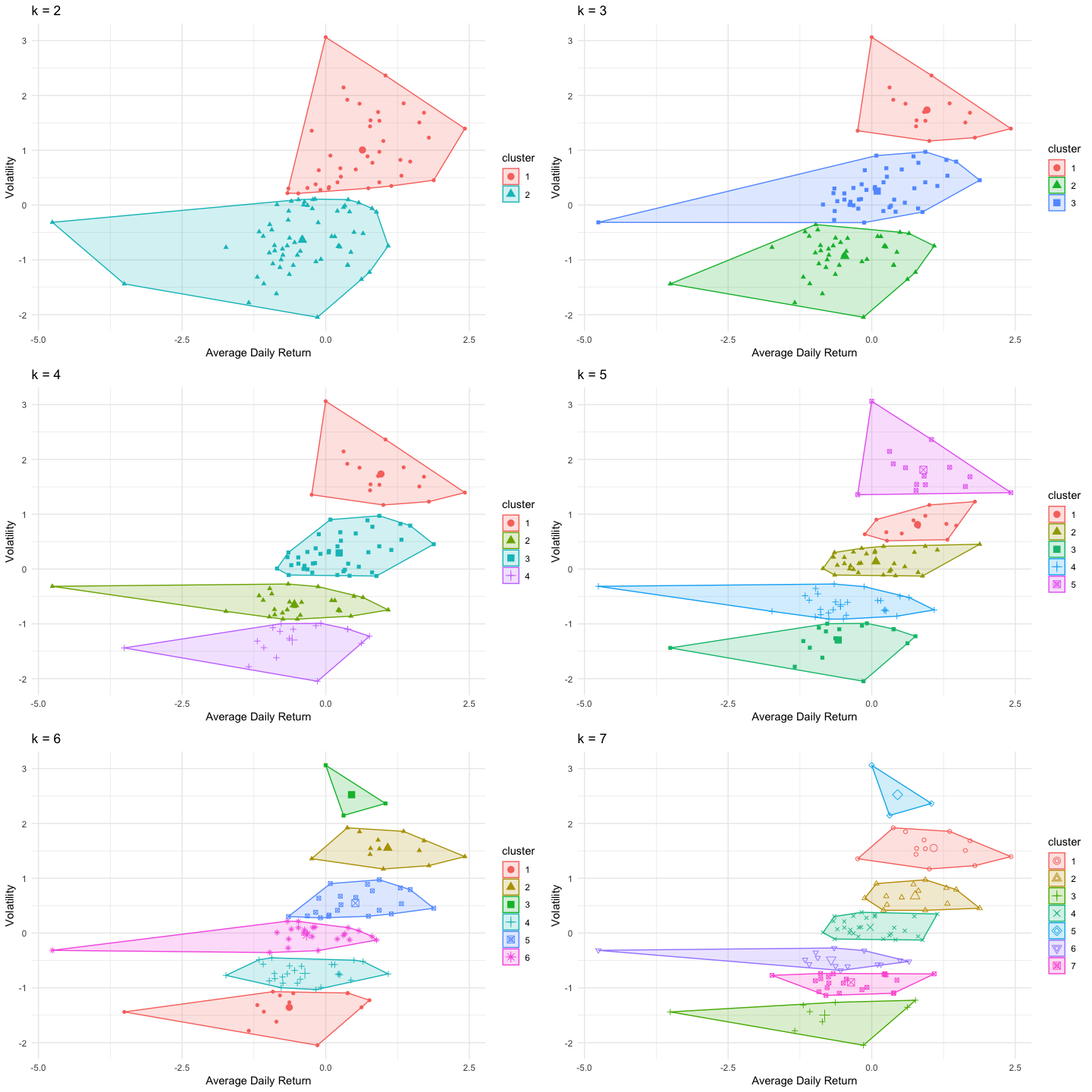

The selected algotrithm for this analysis is the K-Means, which is a fast method to group similar cases. We will perform several analysis, with different k values to identify a good solution.

# Run K-means algorithms with different k values

set.seed(1410)

k2 <- kmeans(stock_return_stats[,c('daily_return_mean','daily_return_sd')],centers = 2, nstart = 25)

k3 <- kmeans(stock_return_stats[,c('daily_return_mean','daily_return_sd')], centers = 3, nstart = 25)

k4 <- kmeans(stock_return_stats[,c('daily_return_mean','daily_return_sd')], centers = 4, nstart = 25)

k5 <- kmeans(stock_return_stats[,c('daily_return_mean','daily_return_sd')], centers = 5, nstart = 25)

k6 <- kmeans(stock_return_stats[,c('daily_return_mean','daily_return_sd')], centers = 6, nstart = 25)

k7 <- kmeans(stock_return_stats[,c('daily_return_mean','daily_return_sd')], centers = 7, nstart = 25)

# Add cluster values in dataset

stock_return_stats$cluster_k2 <- as.factor(k2$cluster)

stock_return_stats$cluster_k3 <- as.factor(k3$cluster)

stock_return_stats$cluster_k4 <- as.factor(k4$cluster)

stock_return_stats$cluster_k5 <- as.factor(k5$cluster)

stock_return_stats$cluster_k6 <- as.factor(k6$cluster)

stock_return_stats$cluster_k7 <- as.factor(k7$cluster)

Analysis

From these charts and the number of cases per cluster shown in the table below, we can already eliminate k=2, k=6 and k=7: * k=2 generates clusters which seem too large, * k=6 and k=7 generates clusters with only a few cases.

| k = 2 | k = 3 | k = 4 | k = 5 | k = 6 | k = 7 |

|---|---|---|---|---|---|

| 40, 63 | 16, 42, 45 | 16, 28, 42, 17 | 13, 31, 17, 28, 14 | 14, 13, 3, 27, 22, 24 | 13, 14, 9, 28, 3, 14, 22 |

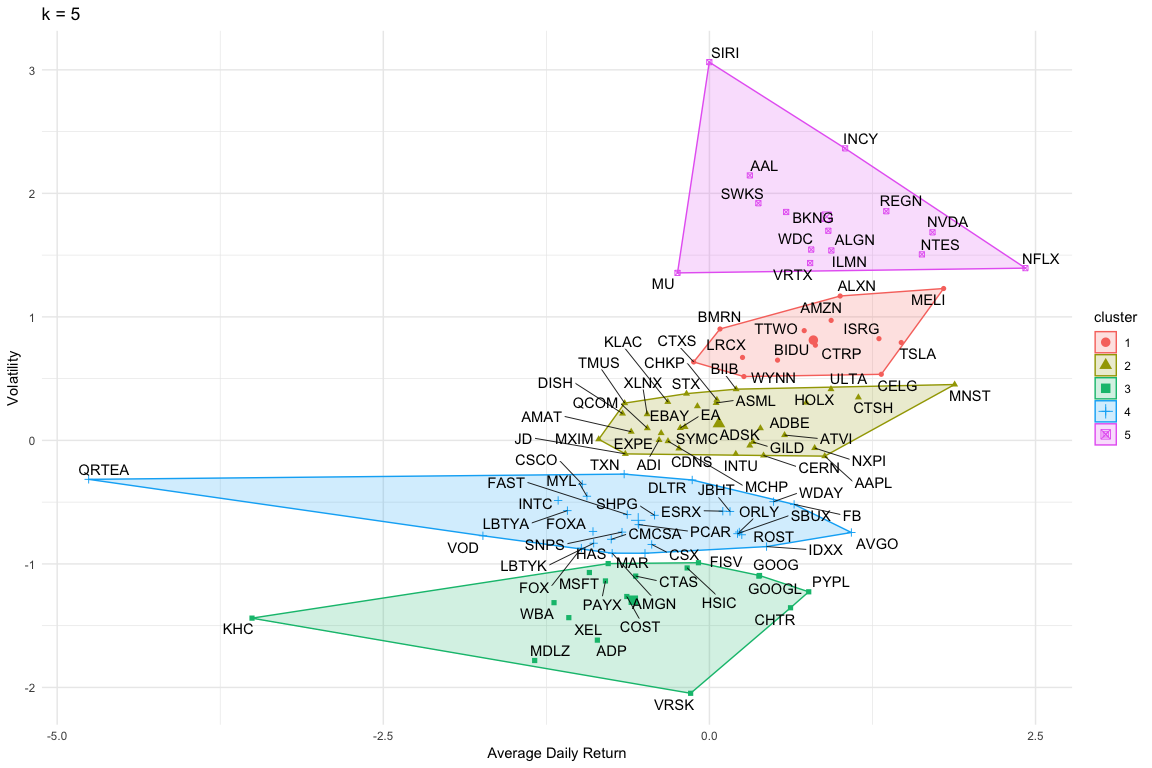

The choice between k=3, k=4 and k=5 is a bit harder, but we would select k=5 as it shows clusters with more balanced numbers of cases. The detailled results of the K-Mean algorithm with k=5 are:

## K-means clustering with 5 clusters of sizes 13, 31, 17, 28, 14

##

## Cluster means:

## daily_return_mean daily_return_sd

## 1 0.0012164960 0.03265923

## 2 0.0008815449 0.02783510

## 3 0.0005778579 0.01763856

## 4 0.0005952686 0.02225341

## 5 0.0012637262 0.03978417

##

## Clustering vector:

## [1] 5 2 2 2 3 2 5 1 2 4 1 2 2 4 1 2 5 1 2 1 2 2 3 4 3 4 4 3 1 2 1 2 4 2 2

## [36] 4 2 4 4 3 4 4 2 3 3 3 2 3 4 5 5 4 2 1 4 2 3 2 4 4 1 4 2 3 1 2 3 5 2 4

## [71] 5 5 5 2 4 3 4 3 2 4 5 4 4 4 5 4 2 5 2 2 1 1 4 2 4 3 5 3 4 5 1 3 2

##

## Within cluster sum of squares by cluster:

## [1] 3.060778e-05 5.399926e-05 7.459454e-05 5.610184e-05 1.432141e-04

## (between_SS / total_SS = 93.1 %)

##

## Available components:

##

## [1] "cluster" "centers" "totss" "withinss"

## [5] "tot.withinss" "betweenss" "size" "iter"

## [9] "ifault"

Looking at the clusters in more details, we can see which companies are grouped together by the algorithm:

| Cluster 1 | Cluster 2 | Cluster 3 | Cluster 4 | Cluster 5 |

|---|---|---|---|---|

| Alexion Pharmaceuticals Inc | Apple Inc | Automatic Data Processing Inc | Amgen Inc | American Airlines Group Inc |

| Amazon.com Inc | Adobe Inc. | Charter Communications Inc | Broadcom Inc | Align Technology Inc |

| Baidu Inc | Analog Devices Inc | Costco Wholesale Corp | Comcast Corp | Booking Holdings Inc |

| Biomarin Pharmaceutical Inc | Autodesk Inc | Cintas Corp | Cisco Systems Inc | Illumina Inc |

| Celgene Corp | Applied Materials Inc | Fiserv Inc | CSX Corp | Incyte Corp |

| Ctrip.Com International Ltd | ASML Holding NV | Alphabet Class C | Dollar Tree Inc | Micron Technology Inc |

| Citrix Systems Inc | Activision Blizzard Inc | Alphabet Class A | Express Scripts Holding Co | Netflix Inc |

| Intuitive Surgical Inc | Biogen Inc | Hasbro Inc | Fastenal Co | NetEase Inc |

| Lam Research Corp | Cadence Design Systems Inc | Henry Schein Inc | NVIDIA Corp | |

| MercadoLibre Inc | Cerner Corp | Kraft Heinz Co | Twenty-First Century Fox Inc | Regeneron Pharmaceuticals Inc |

| Tesla Inc | Check Point Software Technologies Ltd | Mondelez International Inc | Twenty-First Century Fox Inc | Sirius XM Holdings Inc |

| Take-Two Interactive Software Inc | Cognizant Technology Solutions Corp | Microsoft Corp | IDEXX Laboratories Inc | Skyworks Solutions Inc |

| Wynn Resorts Ltd | DISH Network Corp | Paychex Inc | Intel Corp | Vertex Pharmaceuticals Inc |

| Electronic Arts | PayPal Holdings Inc | J.B. Hunt Transport Services Inc | Western Digital Corp | |

| eBay Inc | Verisk Analytics Inc | Liberty Global PLC | ||

| Expedia Group Inc | Walgreens Boots Alliance Inc | Liberty Global PLC | ||

| Gilead Sciences Inc | Xcel Energy Inc | Marriott International Inc | ||

| Hologic Inc | Mylan NV | |||

| Intuit Inc | O’Reilly Automotive Inc | |||

| JD.com Inc | PACCAR Inc | |||

| KLA-Tencor Corp | Qurate Retail Inc | |||

| Microchip Technology Inc | Ross Stores Inc | |||

| Monster Beverage Corp | Starbucks Corp | |||

| Maxim Integrated Products Inc | Shire PLC | |||

| NXP Semiconductors NV | Synopsys Inc | |||

| Qualcomm Inc | Texas Instruments Inc | |||

| Seagate Technology PLC | Vodafone Group PLC | |||

| Symantec Corp | Workday Inc | |||

| T-Mobile US Inc | ||||

| Ulta Beauty Inc | ||||

| Xilinx Inc |

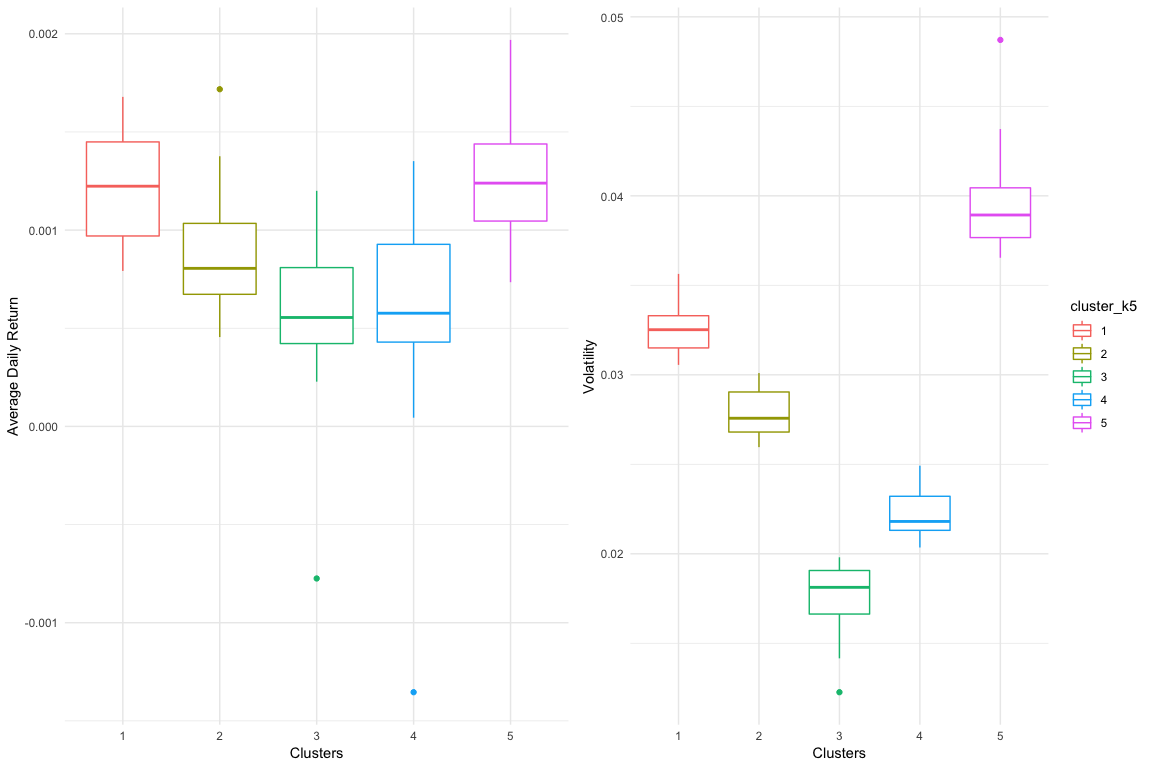

The boxplot below shows how the clusters have been designed considering the Average Daily Return and Volatility values of each case:

The Volatily seems to hav been the clear differentiator of the groups, while the Average Daily Return can be overlapping for several groups. However, it is possible to describe each cluster based on these parameters:

| Parameter | Cluster 1 | Cluster 2 | Cluster 3 | Cluster 4 | Cluster 5 |

|---|---|---|---|---|---|

| Av. Daily Return | High | High | Low/Negative | Low | Low |

| Volatility | High | Very High | Low | Medium | Medium |

Conclusions

This cluster analysis can help investors to identify in which companies they should invest for their long-term investments, based on their profile and risk aversion.

The clusters 1 and 2 have high Average Daily Returns but

also high Volatilities. Individuals willing to invest in these

companies should be will to take higher risk and accept to see their

capital decrease and increase quickly. It is particularly true for the

companies in Cluster 2, like Western Digital, as they have a higher

Volatility but don’t seem to provide the corresponding effect in

returns.

The clusters 4 and 5, in comparison, have low Average Daily

Returns but medium Volatilities. These companies would be

perfect fits for wiser profiles. People liking risk slightly more could

invest in companies of cluster 4, like Apple, in order to get

higher returns.

The cluster 3 seems to list the companies to avoid. These are very

stable with very low Volatilities, but their Average Daily

Return is also very low, and even sometimes negative, like

Verisk Analytics!

Overall, the clusters 2 and 4 seem to be the most attractive, as

they offer a fairly good balance between risk and return.